by Ananta Mukerji

The makers of cars, trucks and other vehicles account for between 40% and 45% of the warranty expenses of all US-based manufacturers. Fraudulent warranty claims therefore represent a significant exposure for Automotive OEMs, and it is important to understand these expenditures in order to estimate the potential savings by implementing an effective system to detect and combat warranty fraud.

This report is based on data published by Warranty Week magazine and it tracks the warranty expenses of 50 US-based automotive OEMs for the past 16 years, by examining their annual reports and quarterly financial statements. The list includes car, light truck, and SUV manufacturers such as Ford and General Motors as well as heavy truck and bus manufacturers such as Navistar and Paccar. It also includes agricultural and construction machinery manufacturers such as Deere and Caterpillar as well as recreational vehicle manufacturers such as Winnebago. Not included are all the foreign parent companies that have US subsidiaries, whose parent companies report their warranty expenses in their own annual reports, in their native currencies. So even though BMW, Volkswagen, Hyundai, Toyota and Honda are among the companies that manufacture vehicles within the United States, and in some cases export them to other markets, they’re not included. Nor is Fiat Chrysler Automobiles, which is based in Europe and reports its expenses in euro.

The 50 OEMs are grouped here into 2 groups, Small and Large, by the size of the vehicles they produce. Small includes 24 manufacturers of passenger cars, motorcycles, SUVs, ATVs, pickup trucks, vans, snowmobiles, riding lawn mowers, golf carts, and motorized bikes and scooters. Large includes 26 manufacturers of heavy trucks, medium trucks, vocational vehicles, emergency vehicles, buses, RVs, construction equipment, farm equipment, and road paving vehicles.

All the companies report just one set of warranty expense figures for all their product lines, and for both their domestic sales and exports, as well as their overseas production, if any. So it is not possible for an external observer to determine the precise warranty cost of a Ford F-150 pickup truck or a Tesla Model 3. All the totals and averages apply to the companies as a whole.

Total Warranty Claims

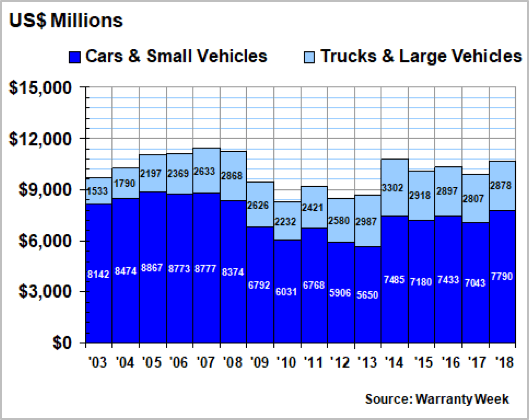

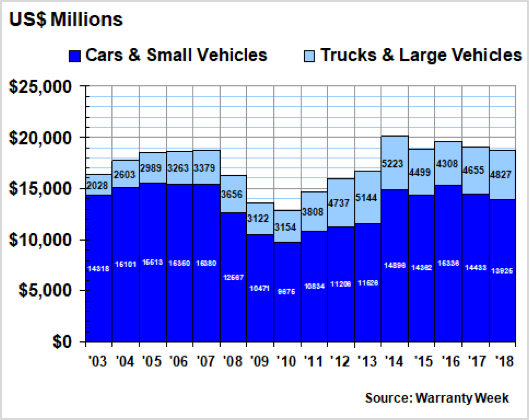

Figure 1 (right) depicts the total warranty claims expenses over a 16-year period from 2003 thru 2018. Note that the 16-year period can be divided into basically three periods: six years before the recession (to 2008), five years of recession (to 2013), and the five years since (to 2018).

In 2018, the car and small vehicle manufacturers reported $7.79 billion in claims payments, up by $747 million or 11% from 2017 levels. The truck and large vehicle manufacturers, meanwhile, reported $2.88 billion in claims payments, up by $71 million or 2.5% from 2017 levels.

In most years, the small vehicle makers account for about three-quarters of the industry total for all OEMs. In 2018, they accounted for 73% of the $10.67 billion claims total — slightly below their long-term average but above the share they’ve held for the past six years. That’s because their claims total grew much faster than the truck manufacturers’ did last year

Figure 1: Automotive OEM Warranty Claims Paid by US-based Companies (in US$ millions, 2003-2018)

Warranty Accrual Totals

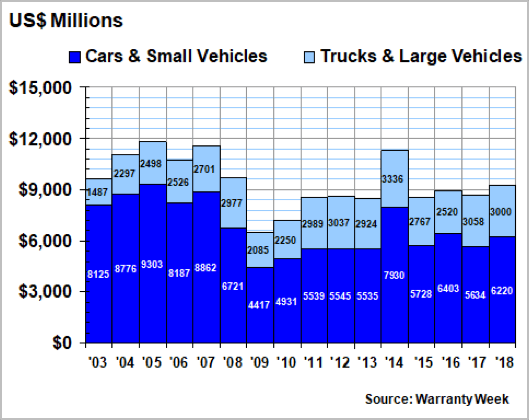

Figure 2 (right) depicts the warranty accruals reported by the automotive OEMs. These are the amounts they set aside at the time of sale, to finance the expected cost of warranty in the future.

Usually, over the long term, accruals approximate the claims totals, although there are lots of ways they can differ. For instance, when sales are soaring or plummeting, there’s a mismatch caused by the lag time between claims and accruals. During the recession, warranty work on older vehicles became more important, and since sales were down, so were accruals. So in Figure 2, the trough is deeper in 2009 and 2010.

Also, accruals are more sensitive to safety recalls. For instance, in 2014 GM disclosed its ignition switch problems and initiated a massive and expensive recall. And that led to a one-year multi-billion-dollar jump in accruals, which was gradually spend over the next several years on claims. So that’s why 2014 is the dividing line between the recession and recovery phases of Figure 1 and why it’s the anomaly among the past eight years in Figure 2.

In 2018, the small vehicle makers accrued $6.22 billion, up $586 million or 10% from their 2017 totals. The large vehicle makers accrued exactly $3 billion, down by $58 million or -1.9% from their 2017 totals. The industry as a whole accrued $9.22 billion, which, excepting 2014, was their first year above $9 billion since 2008.

Figure 2: Automotive OEM Warranty Accruals Made by US-based Companies (in US$ millions, 2003-2018)

Warranty Expense Rates

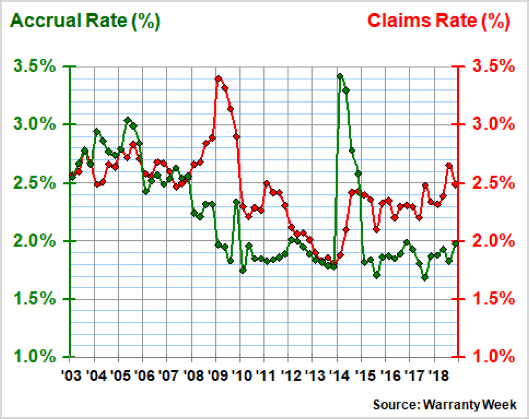

Absent any extraordinary events, accruals should be proportional to sales, since the manufacturers are predicting the future cost of warranty at the time of sale. No sale, no warranty. And if there’s been no change in either the frequency or the cost of warranty work, there should be no change in the predicted total cost. In Figure 3 and 4 we take the claims and accrual totals from Figures 1 and 2 and compare them to sales. As such, each pair of lines provides the ratio between claims and sales, and accruals and sales, for both the small vehicle makers (Figure 3) and the large vehicle makers (Figure 4).

In Figure 3, the two most peculiar features are the 2009 spike in the claims rate, and the 2014 spike in the accrual rate. The 2014 spike is due to the previously mentioned ignition switch problems at GM. The 2009 spike, meanwhile, is due to the recession, but not because of a jump in claims — it was a sudden drop in sales that caused the ratio to climb to 3.4%.

The data is in a quarterly format, as it makes the averages more meaningful, since they’re calculated every three months instead of just once a year.

In Figure 3, the long-term average claims rate of the small vehicle makers is 2.5%, with a standard deviation of 0.33%. The long-term average accrual rate of the small vehicle makers is 2.2%, with a standard deviation of 0.45%.

The space between them, as mentioned, is filled through changes in estimate, where the manufacturer adds extra funds to their warranty reserve fund to correct past under-accruals. In 2018, this gap was significant, with the small vehicle claims rate coming in at 2.5% and the small vehicle accrual rate just under 2.0%.

Figure 3: Car & Small Vehicle Makers Average Warranty Claims & Accrual Rates (as a % of product sales, 2003-2018)

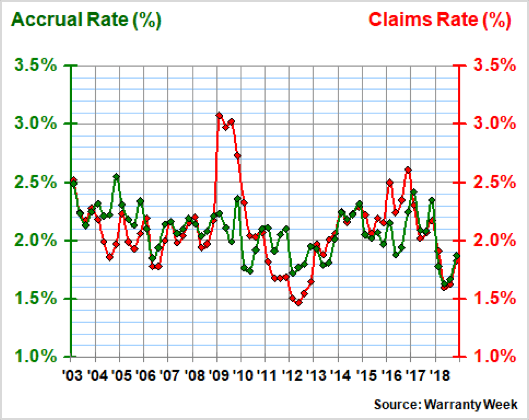

In Figure 4 (right), it’s instantly apparent that the truck and large vehicle manufacturers spend a smaller percentage of their sales revenue on warranties. Both their claims and accrual rates have averaged 2.1% over the long term, with much lower standard deviations than the other group as well. That’s because, while they did experience the recessionary spike in their average claims rates, they did not feel the pain of the ignition switch recall in 2014. So there was no spike in their accrual rates.

Figure 4: Truck & Large Vehicle Makers Average Warranty Claims & Accrual Rates (as a % of product sales, 2003-2018)

Warranty Accrual Totals

Our final metric is the closing balance left in the warranty reserves of these 50 automotive OEMs at the end of each year. Once again, we’ve separated them into two lists, for large and small vehicles. And once again, the small vehicle makers account for the bulk of the funds.

However, while for accruals the ratio between the totals for the small and large OEMs is close to two-to-one, and for claims it’s three-to-one, for reserves it has approached and even exceeded four-to-one over the past 16 years.

In 2018, the small vehicle makers ended the year with $13.925 billion in their warranty reserve funds, a decrease of $508 million or -3.5% from 2017 totals. The large vehicle makers ended the year with $4.827 billion in their warranty reserve funds, an increase of $172 million or 3.7% from the previous year.

Taken together, the large and small vehicle OEMs held $18.752 billion in their warranty reserve funds at the end of 2018, with a ratio of three-to-one between the small and large vehicle makers. From 2003 to 2007, the small vehicle OEMs held in excess of 80% of the industry’s combined reserves. Only in 2013 did their share ever dip below 70%.

Figure 5: Automotive OEM Warranty Reserves Held by U.S.-based Companies (in US$ millions, 2003-2018)

Overall Trends

Bottom line, what it all means is this: none of the warranty metrics are currently at the high end of their historic ranges. In fact, for warranty reserves, 2018 represented only the sixth-highest total of the last 16 years. Accruals are at the high end of an eight-year trend, but they have been both much higher and much lower in the years before. Claims have remained more or less stable for five years running, and are still below their 2005-to-2008 peak levels.

When we look at the industry’s warranty expense rates, we see the percentages creeping up for the small vehicle makers and creeping down for the large vehicle makers, but no clear long-term trends. Meanwhile the unseen metric is sales, with both unit sales and product revenue at or near record highs in recent years. In other words, the manufacturers are making more products than ever before, while spending the same or a lower percentage on warranty work. And that’s good news for the automotive industry.